Are you prepared for the invasion of Zombie debt? Everyone knows there is a foreclosure crisis – but are we prepared for the unfolding crises of education and medical debt?

Student debt is the looming crisis . In his recent NY Times blog, “Student Debt and the Crushing of the American Dream,” economist Joseph Stiglitz notes some astounding facts:

According to the Federal Reserve Bank of New York, almost 13 percent of student-loan borrowers of all ages owe more than $50,000, and nearly 4 percent owe more than $100,000. These debts are beyond students’ ability to repay, (especially in our nearly jobless recovery); this is demonstrated by the fact that delinquency and default rates are soaring. Some 17 percent of student-loan borrowers were 90 days or more behind in payments at the end of 2012. When only those in repayment were counted — in other words, not including borrowers who were in loan deferment or forbearance — more than 30 percent were 90 days or more behind. For federal loans taken out in the 2009 fiscal year, three-year default rates exceeded 13 percent.

The high cost of higher education, interest rates and the laws governing student loans (removing them from bankruptcy and other debt relief programs), and relatively high unemployment all contribute to lowering economic and social opportunity/mobility. Despite the debate – the “value added” by a college degree is still clear. Stiglitz notes the numbers:

College graduates earn $12,000 more per year than those without college degrees; the gap has almost tripled just since 1980. Our economy is increasingly reliant on knowledge-related industries. No matter what happens with currency wars and trade balances, the United States is not going to return to making textiles. Unemployment rates among college graduates are much lower than among those with only a high school diploma.

Contributing to the crisis are predatory practices by for profit colleges, with high default rates and low graduation rates, as well as, the broader economic reality. Overwhelming student debt and higher unemployment lowers consumption (and in a consumer economy, this creates a circular problem). Stiglitz’s main point is that the looming student debt crisis is not a failure of students, it is a failure of our public commitment to education and social mobility (something he has written about elsewhere).

There is a structural injustice at the root of this problem. Banking fraud and illegal foreclosures continue (without any real threat of punishment). A culture of fraud extends beyond the foreclosure crisis into medical and education debt. (on the education side, this fraud is perpetuated by for-profit institutions with high loans, low graduation/completion rates, and high probability of default). This structural component is at the heart of the biblical jubilee and justice tradition, which calls for the forgiveness of debts.

Within this reality, however, a group of people fighting back – Rolling Jubilee by Strike Debt began its campaign to cancel the debts of individuals. Linking the jubilee tradition in Judaism, Islam and Christianity, RollingJubilee.org

Strike Debt is an offshoot of Occupy Wall Street. First started in New York City, but inspired by movements around the globe, Strike Debt now has affiliates across the country. We believe people should not go into debt for basic necessities like education, healthcare and housing.

Beginning with medical and housing debt – Strike Debt buys individual debt and cancels or “forgives the debt.” How do they do this? What most people do not know that defaulted debt is sold on a secondary market – bundled together and sold at auction.

Banks sell debt for pennies on the dollar on a shadowy speculative market of debt buyers who then turn around and try to collect the full amount from debtors. The Rolling Jubilee intervenes by buying debt, keeping it out of the hands of collectors, and then abolishing it. We’re going into this market not to make a profit but to help each other out and highlight how the predatory debt system affects our families and communities. Think of it as a bailout of the 99% by the 99%

In many of these cases, the patients are haunted by Zombie Debt, or debts they thought were paid off.

Logsdon, the first of those debtors to publicly identify herself, said she thought her delinquent $983 bill for back pain care had been paid by Medicare last year. That’s what her doctor told her, she said, after a 2011 dispute during which the bill had gone to a collection agency.

Strike Debt has forgiven 1.1 million in medical loans and they are now investigating ways they can buy and cancel student loans. Federally backed student loans do not get sold on a secondary market, but an increasing number of defaulted private loans are making their way to the secondary market.

In Luke’s Gospel, Jesus stands up and reads from Isaiah and explains his purpose. He has come to proclaim liberty to captives, to let the oppressed go free, and to proclaim a year acceptable to the Lord. Deeply embedded in the Biblical tradition is the concept of Jubilee – what does it mean to set people free and proclaim a year acceptable to the Lord?

The Jubilee tradition understands biblical justice to include the forgiveness of debts. Rolling Jubilee is following the legacy of Jubilee 2000. During the Millennium, Pope John Paul II, Bono and others mobilized the world around the Jubilee 2000 Campaign and the forgiveness of crippling loans to developing countries. While the fight for debt relief for developing countries goes on, it has also accomplished a lot of good for the citizens of developing countries – by freeing up money for investment in public goods. Jubilee is necessary to proclaim a year acceptable to the Lord. There is strong theological support for Rolling Jubilee’s forgiveness of medical debt and perhaps it is time to call for a Jubilee for student debt as well.

*edited to clarify the for-profit versus non-profit education reality.

Meg– Ordinarily, I am in strong agreement with your interpretation and application of CST, but I take significant exception on the issue of student debt. Raw statistics are not helpful here. As this NPR Marketplace report, linked to an Atlantic piece, shows, student debt is almost always manageable and a “good deal.” http://www.marketplace.org/topics/economy/education/wait-we-dont-have-student-debt-crisis The aggregate numbers mask and distort the extent to which the problem is opportunistic for-profit colleges enrolling students, taking their money (really, the loans), and not graduating them. As this Department of Education report on the problem shows, the 3-year default rate for private non-profit colleges is 7.5%, compared to an astonishing 22.7% AVERAGE default rate at for-profit colleges. http://www.ed.gov/news/press-releases/first-official-three-year-student-loan-default-rates-published

This links you to a database where you can look at particular institutions. http://studentaid.ed.gov/about/data-center/student/default You will see that standard four-year colleges, private and public, have very low default numbers, almost always in the single digits. This is because our students grauadte and are employed. This is not just true of wealthy institutions. But if you look at the schools with 20%+ default rates, you see the for-profits and beauty academies… a lot of beauty academies. Even a “reputable” for-profit like University of Phoenix, which enrolled over 350000 students (not a misprint), has a 3-year deafult rate of over 21%.

If you look at the Chronicle’s comprehensive survey of college completion rates, you will find that onling schools have a terrible completion rate, most falling well below 40%, some much lower than that. http://collegecompletion.chronicle.com/table/

It is deeply embarrassing that these poor-performing schools get away with this kind of “performance.” This Frontline video is required viewing for anyone who wants to see their tactics: http://www.pbs.org/wgbh/pages/frontline/collegeinc/view/

This is sheer profiteering, and if there is structural injustice involved, it is the inability of the academic and government structures to shut these scams down. But they are scams, and students should not choose to enroll if they are not going to complete a degree.

Overall, I think the “student debt bubble” rhetoric conflates good and bad debt, and makes it sound like there is some awful onus hanging over all college students. It’s not true. The statistics clearly show that the recent “explosion” is due to bad for-profits with horrible completion rates. Shut them down.

Let me add to what David says. I lifted these stats from American Student Assistance:

Among all bachelor’s degree recipients, median debt was about $7,960 at public four-year institutions, $17,040 at private not-for-profit four-year institutions, and $31,190 at for-profit institutions. (Source: College Board)

Don’t take them as the final truth, but they more or less match what I read a while ago in either the Washington Post or the Chronicle of Higher Education but couldn’t locate by searching (this is why blog posting is so much easier than research for publication!). $8,000 or $17,000 is manageable for most young people who have a 4-year degree from an accredited college. The problems lie with the for-profits and with outliers. The biggest mistake–and I have personally known students who made it–is to take all the loan money that is offered, rather than simply what one needs for their education. If we could change one thing, that would seem to be it.

David –

I agree with you completely about for profit colleges and their default rate. They are predatory. They should be shut down – and on one level, I agree with you about good debt. We agree about schools without satisfactory completion rates as well. (and I wouldn’t call university of phoenix reputable -their default and retention/graduation rates are awful! as you note). They should be shut down! But maybe we should do something about the debt they got students into (without much to show for it) too?

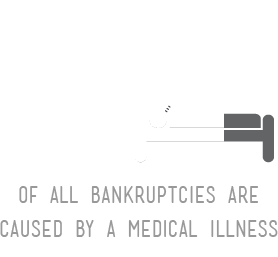

The point that I was trying to make and that Stiglitz and others (including Strike Debt) is that the way in which we have “good debt” structured perpetuates injustice and lowers social mobility. Medical debt isn’t debt accumulated for doing “bad” things or being beyond one’s means. One can do everything right and still easily end up in bankruptcy due to cancer.

The problem with simply looking at student debt as unqualified “good debt” is I think two fold. 1. we have a general financing and affordability of higher education problem. 2. We have a significant youth unemployment or under-employment problem – this is significantly higher for those without a college degree but it is rising for college graduates (but thank GOD we are not in Europe’s youth unemployment situation). But the “student debt bubble” does exist has a number of consequences beyond simply default –

~More and more young adults are moving back home with their parents because with full time jobs they cannot afford to pay rent and student loans. I know many people intentionally delaying marriage and children because of student loans. whether that is smart or not – it is a growing reality.

~Contributes to our inability to get teachers, doctors, lawyers, and other professionals in low income areas of the country – no one goes into general medicine because in part, because paying off their loans is easier in high cost specialties. (Money driven medicine is an excellent POV documentary on this).

~ If you want to work in Catholic schools, as a social worker, as a community organizer, for a non-profit……you can’t unless you do not have or have very little in student loans. These jobs, which are so important, do not pay enough to be an independent adult and pay the loans.

Why I think both Rolling Jubilee (which is canceling medical because most education is not sold on secondary market) and Stiglitz are pointing to is the structural injustice. I think a big part of that structural injustice is wrapped up in cost and debt to the extent that we are talking about very low social and economic mobility in the US. I think we need to think about student debt not only as good debt, but also a matter of public good as well. Calling thus for a significant expansion of programs that allow for the forgiveness of student loans (like americorp)